Yes, you can often keep your home in a Chapter 7 bankruptcy, provided you meet certain requirements related to its value and your equity in it. This guide will walk you through the process and the factors that determine if your home is protected during filing for bankruptcy.

Image Source: www.therollinsfirm.com

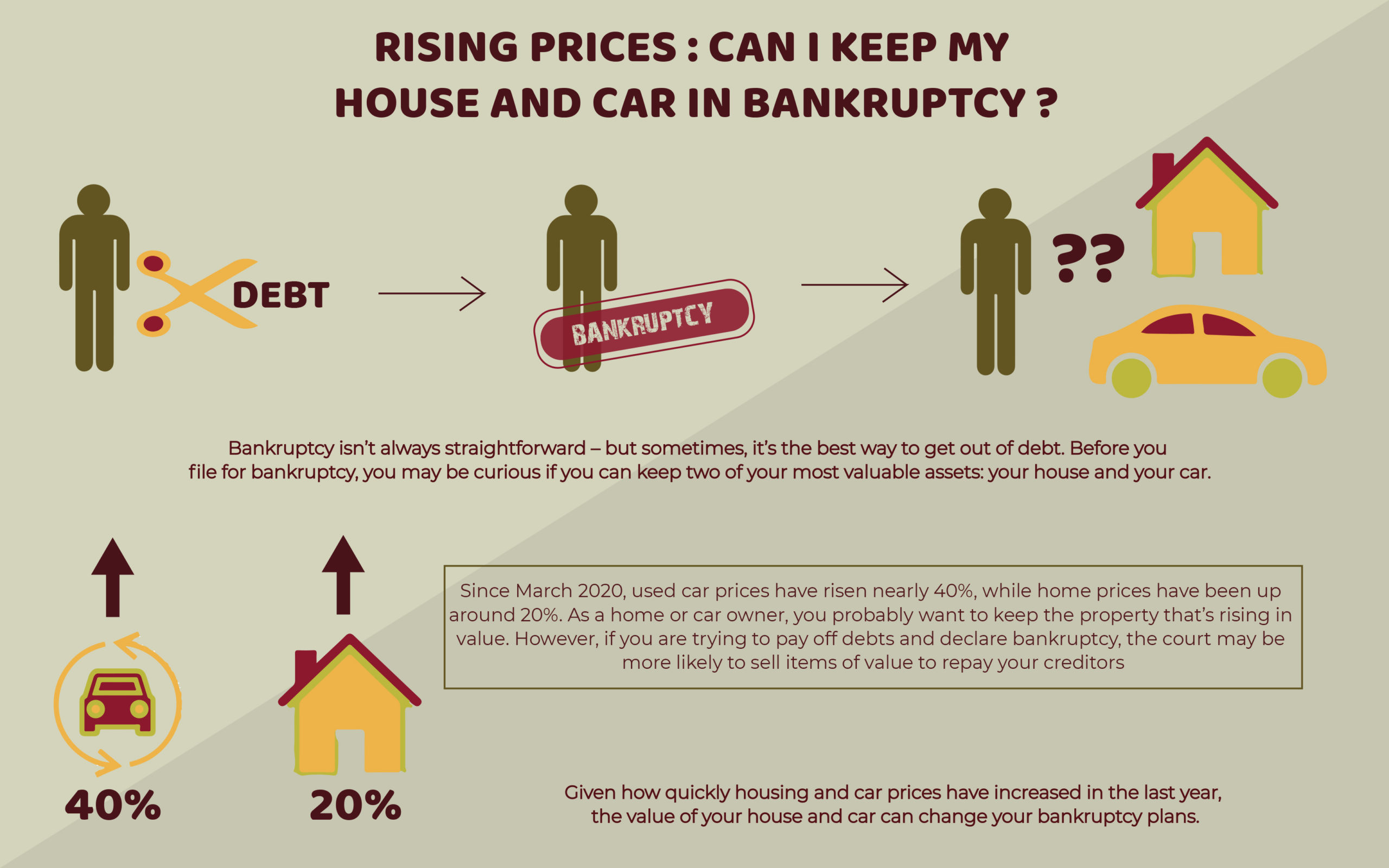

Fathoming Your Home’s Status in Bankruptcy

When you consider filing for bankruptcy, particularly Chapter 7, one of the most pressing questions is about your most valuable asset: your home. Chapter 7 bankruptcy, often called liquidation, involves selling non-exempt assets to pay off creditors. However, not all assets are automatically lost. The key to keeping your home lies in asset protection through exemptions.

The Role of Exemptions

Exemptions are legal provisions that allow you to keep certain property when you file for bankruptcy. These vary significantly by state, and in some cases, you can choose between federal or state exemptions. The most crucial exemption for homeowners is the Homestead exemption.

The Homestead Exemption Explained

The Homestead exemption protects a certain amount of equity in your primary residence. This means that if the value of your home, minus any outstanding mortgage or liens, falls within the exemption amount, your home is generally safe from liquidation.

How Equity Works:

- Home Value: What your home is currently worth on the market.

- Mortgage Balance: The total amount you still owe on your mortgage.

- Equity: Home Value – Mortgage Balance.

Example:

If your home is worth $300,000 and you owe $200,000 on your mortgage, your equity is $100,000. If your state’s Homestead exemption is $75,000, and you have $100,000 in equity, $25,000 of that equity would be considered non-exempt and potentially liquidated to pay creditors.

State-Specific Exemptions

It’s vital to know your state’s exemption laws. Some states offer very generous Homestead exemption amounts, while others have more modest limits. Some states even allow unlimited homestead exemptions.

Table: Sample Homestead Exemption Amounts (Illustrative – Laws Change!)

| State | Homestead Exemption Amount |

|---|---|

| Texas | Unlimited |

| Florida | Unlimited |

| California | $100,000 (varies by county) |

| New York | $200,000 (varies by county) |

| Illinois | $20,000 |

| Pennsylvania | $20,000 |

Note: These are examples. Always consult with a bankruptcy lawyer for the most current and accurate information for your specific state.

Federal Exemptions

If your state doesn’t have its own exemption laws or if you qualify to use federal exemptions (which is typically only if you haven’t lived in your state for at least two years), you can use the federal Homestead exemption amounts. These are also subject to change by Congress.

Keeping Your Home When Equity Exceeds Exemptions

What if your home’s equity is more than the available exemption? This is where things get more complex, but there are still potential avenues to keep your home.

Negotiating with the Trustee

In some cases, the bankruptcy trustee might be willing to negotiate with you. If the non-exempt equity is relatively small, the trustee might allow you to “buy back” the non-exempt portion. You would pay the trustee the amount of equity that exceeds the exemption, and in return, the trustee would abandon their claim to that portion of your home.

The Buy-Back Option

This often involves securing a loan or using savings to pay the trustee. It’s a way to leverage asset protection in bankruptcy by using funds to cover the non-exempt equity.

Selling the Home Voluntarily

Another option, if you can’t afford to buy back the non-exempt equity, is to sell the home voluntarily before the trustee is forced to. You can then use the proceeds to pay creditors and keep any remaining equity that is protected by exemptions. This approach can give you more control over the sale process than if the trustee liquidates it.

Secured Debts and Your Home

Your mortgage is a secured debt. This means the lender has a lien on your home, using it as collateral for the loan. When you file for bankruptcy, you have several options for dealing with secured debts like your mortgage.

Reaffirmation Agreement

One way to keep your home and continue paying your mortgage is to enter into a reaffirmation agreement. This is a contract between you and the lender where you agree to remain personally liable for the debt, even though you are receiving a bankruptcy discharge.

Pros of Reaffirmation:

- Keeps your home.

- Allows you to continue making payments as usual.

- May help rebuild credit over time if payments are made on time.

Cons of Reaffirmation:

- You remain responsible for the debt. If you can’t pay in the future, the lender can still foreclose.

- You must demonstrate to the court that reaffirming the debt will not cause you undue hardship.

To reaffirm your mortgage, you generally must be current on your payments at the time of filing.

Keeping the Property Without Reaffirmation (Ride-Through)

In some jurisdictions and for certain types of debts, you may be able to keep the collateral (your home) and continue making payments without formally reaffirming the debt. This is sometimes referred to as a “ride-through.” The idea is that as long as you keep making the payments, the lender cannot repossess or foreclose.

However, it’s crucial to note:

- This option is not available in all districts or for all types of secured debts.

- Lenders may still require reaffirmation or take other actions if you are not current on your payments.

- Consulting with a bankruptcy lawyer is essential to determine if this is a viable option for your situation.

Surrendering the Home

If you can’t afford your mortgage payments, or if the equity exceeds your exemptions and you can’t afford to buy it back, you may choose to surrender your home in Chapter 7 bankruptcy.

Consequences of Surrendering:

- The lender will foreclose.

- Any remaining deficiency balance (the difference between what you owe and what the house sells for) might be discharged as an unsecured debt, depending on state law and the loan terms.

Other Debts and Their Impact

While the focus is often on the home, other debts play a role in the bankruptcy process and your ability to keep your property.

Unsecured Debts

Unsecured debts are those not backed by collateral. Examples include credit card debt, medical bills, and personal loans. In Chapter 7, most unsecured debts are dischargeable. This means that once your bankruptcy is complete, you are no longer legally obligated to pay them.

The discharge of unsecured debts is a primary benefit of Chapter 7. It frees up your income, which can then be used to make mortgage payments or catch up on payments to keep your home.

Secured Debts Other Than Your Mortgage

If you have other secured debts, like a car loan, you generally have similar options: reaffirm the debt, keep the property without reaffirmation (if allowed), or surrender the property. The trustee will only take action on these assets if they are non-exempt and have significant value.

The Concept of Disposable Income

While Chapter 7 is a liquidation bankruptcy, the concept of disposable income is more central to Chapter 13 bankruptcy. However, in Chapter 7, if your income is above the median income for your state, you may be required to pass the “means test,” which assesses your income and expenses. If you have substantial disposable income after essential living expenses, a trustee might scrutinize your situation more closely, or you might be steered towards Chapter 13.

Asset Protection in Bankruptcy

Asset protection in bankruptcy is about strategically using exemptions and legal maneuvers to shield your property from the bankruptcy estate. This isn’t about hiding assets; it’s about utilizing the rights granted by bankruptcy law.

The Bankruptcy Estate

When you file for bankruptcy, all your property in bankruptcy becomes part of the bankruptcy estate, managed by a trustee. The trustee’s job is to liquidate non-exempt assets to pay your creditors. Understanding which assets are exempt is paramount to asset protection in bankruptcy.

What the Trustee Can Take

The trustee can seize and sell any non-exempt assets to pay creditors. This could include:

- Vehicles with significant equity above the vehicle exemption.

- Bank accounts exceeding a certain exemption limit.

- Second homes or investment properties.

- Valuable personal property like jewelry or collectibles beyond exemption limits.

Strategic Planning Before Filing

For effective asset protection in bankruptcy, planning before you file is crucial.

Consulting a Bankruptcy Lawyer

This cannot be stressed enough. A qualified bankruptcy lawyer can:

- Advise you on the best exemption strategy for your state.

- Help you understand your equity in your home and other assets.

- Guide you on the bankruptcy filing requirements.

- Explain the implications of reaffirmation agreements.

- Assist in navigating the complexities of disposable income calculations and the means test.

- Represent you before the court and the trustee.

Timing Your Filing

Sometimes, timing your bankruptcy filing can impact your ability to keep your home. For instance, if you’ve recently taken out equity from your home, that transaction might be subject to scrutiny and could be “clawed back” by the trustee.

Addressing Arrears

If you are behind on your mortgage payments, the situation is more complicated. While Chapter 7 can discharge unsecured debts, it generally does not discharge secured debts like mortgages unless you reaffirm or surrender the property. If you want to keep your home and are behind, you may need to catch up on the arrears, which Chapter 7 alone typically doesn’t facilitate. This is often a reason individuals opt for Chapter 13 bankruptcy, which allows for a repayment plan to catch up on missed payments.

Bankruptcy Filing Requirements

To successfully navigate filing for bankruptcy, you must meet specific criteria.

Eligibility for Chapter 7

- Means Test: As mentioned, you must pass the means test, demonstrating that your income is not high enough to afford a Chapter 13 repayment plan.

- Credit Counseling: You must complete a credit counseling course from an approved agency within 180 days before filing.

- Debtor Education: After filing, you must complete a debtor education course to receive a discharge.

- Honesty and Disclosure: You must truthfully disclose all your assets, liabilities, income, and expenses. Failure to do so can result in the denial of your discharge.

The Automatic Stay

Once you file for bankruptcy, an “automatic stay” immediately goes into effect. This legal injunction stops most creditors from pursuing collection efforts against you, including foreclosures, wage garnishments, and lawsuits. This provides immediate relief and gives you breathing room to organize your financial situation.

Frequently Asked Questions About Keeping Your Home in Bankruptcy

Here are some common questions people have about keeping their homes during bankruptcy:

Q1: What happens to my mortgage if I file for Chapter 7 bankruptcy?

A1: Your mortgage is a secured debt. You have a few options: you can reaffirm the debt, surrender the home, or in some cases, keep it without reaffirmation if you stay current on payments. If you don’t reaffirm and are not current, the lender can typically proceed with foreclosure after the automatic stay is lifted.

Q2: Can the bankruptcy trustee sell my home?

A2: The trustee can only sell your home if it contains non-exempt equity. If the equity in your home is fully covered by your applicable Homestead exemption, the trustee generally cannot sell it.

Q3: What if my home’s equity is more than the exemption amount?

A3: If your equity exceeds the exemption, the trustee can sell the home. However, you may be able to keep it by:

* Paying the trustee the amount of non-exempt equity.

* Negotiating with the trustee.

* Choosing to sell the home yourself to retain the exempt portion of the equity.

Q4: Does Chapter 7 bankruptcy stop foreclosure?

A4: Yes, the automatic stay that goes into effect immediately upon filing for bankruptcy will temporarily stop foreclosure proceedings. However, this is a temporary reprieve. To keep your home long-term, you must address the mortgage debt through reaffirmation or by bringing payments current.

Q5: What is asset protection in bankruptcy?

A5: Asset protection in bankruptcy refers to the legal right to keep certain possessions, like a portion of your home’s equity through the Homestead exemption, from being sold by the bankruptcy trustee to pay creditors.

Q6: Can I get rid of my mortgage in Chapter 7?

A6: You cannot “get rid of” a mortgage in Chapter 7 in the same way you can discharge an unsecured debt. You must either continue paying it (often through reaffirmation), surrender the home, or pay off the equity that is not protected by exemptions.

Q7: What are the bankruptcy filing requirements?

A7: Key bankruptcy filing requirements include passing the means test (for Chapter 7), completing mandatory credit counseling and debtor education courses, and providing accurate and complete financial disclosures.

Q8: How does disposable income affect my ability to keep my home?

A8: While Chapter 7 is not income-based, a high level of disposable income might mean you don’t qualify for Chapter 7 and would be better suited for Chapter 13. In Chapter 13, disposable income is crucial for determining your repayment plan.

Q9: What is a bankruptcy lawyer?

A9: A bankruptcy lawyer is an attorney specializing in bankruptcy law. They provide legal advice and representation to individuals and businesses filing for bankruptcy, helping them understand their rights and navigate the complex legal process.

Q10: What are secured debts?

A10: Secured debts are loans where the borrower has pledged collateral to guarantee repayment. If the borrower defaults, the lender can seize the collateral. Mortgages and car loans are common examples of secured debts.

Q11: What are unsecured debts?

A11: Unsecured debts are not backed by collateral. If the borrower defaults, the lender has no specific asset to seize. Common examples include credit card debt, medical bills, and personal loans.

Q12: How can I protect my home from creditors outside of bankruptcy?

A12: While this guide focuses on bankruptcy, other asset protection strategies exist, such as certain types of trusts or pre-paid legal services, but these are complex and have specific rules. Within bankruptcy, the Homestead exemption is the primary tool for home asset protection.

Conclusion: Navigating Your Path to Homeownership Protection

Deciding whether to file for bankruptcy and how to protect your home requires careful consideration and professional guidance. By understanding Homestead exemptions, the nature of secured debts and unsecured debts, and the overall bankruptcy filing requirements, you can make informed decisions. Consulting with an experienced bankruptcy lawyer is your most critical step. They can provide personalized advice, ensure you are utilizing the best asset protection strategies available, and help you achieve the best possible outcome for your financial future, potentially allowing you to keep your home even after filing for bankruptcy.